CalHome vs SDHC for First-Time Buyers in San Diego: Closing Costs & Loans Explained for 2026

CalHome vs SDHC for First-Time Buyers in San Diego: Closing Costs & Loans Explained for 2026

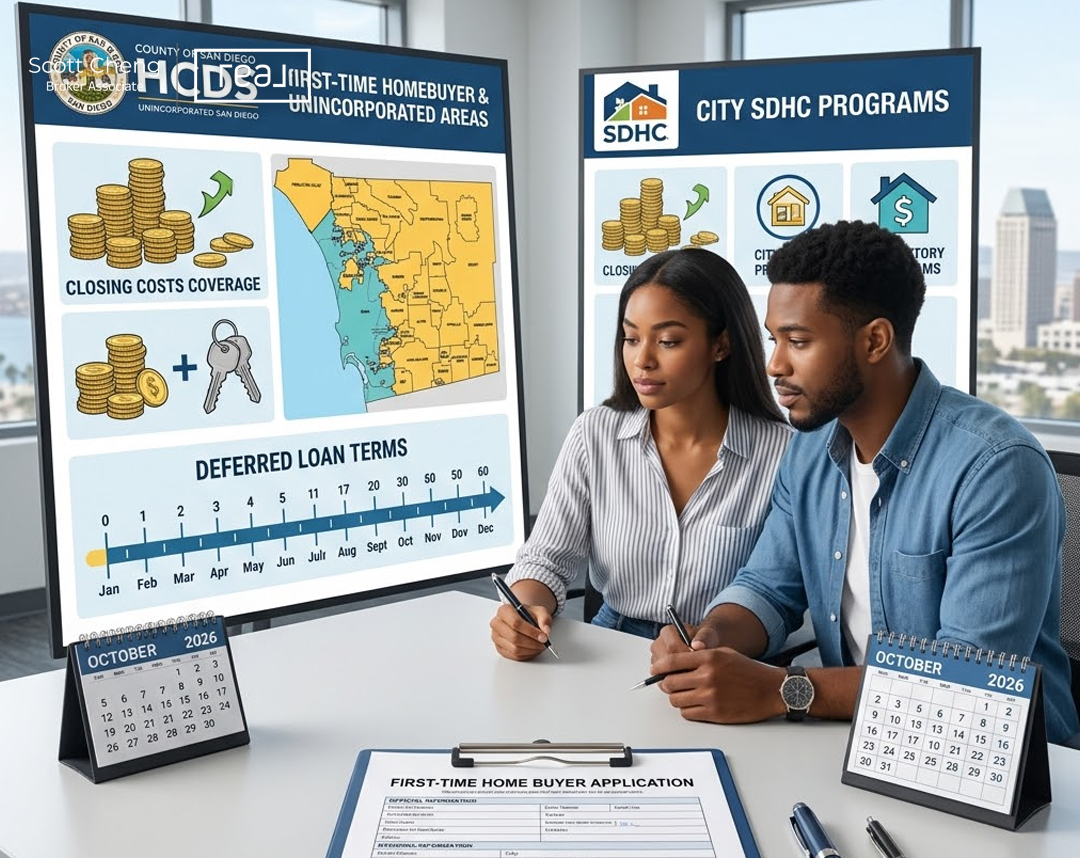

The County CalHome grant typically covers more pure closing costs in unincorporated areas, up to $15,000, while SDHC programs generally offer larger deferred loans, often $50,000 to $100,000, that can cover down payment and some closing fees when eligible.

Why Does This Matter for San Diego First-Time Buyers Right Now?

San Diego’s seller’s market — with just 2.8 months of inventory as of January 2026 and a county median near $850,000 — means every dollar of grant or deferred loan assistance directly affects your ability to compete. With rates around 6.75 to 7.0 percent reducing purchasing power, comparing County CalHome to SDHC programs before you apply helps you make a confident, competitive offer. In unincorporated San Diego, your path to affordability can look different than inside city limits, which is why this comparison matters whether you are focused on Spring Valley or considering nearby La Mesa and El Cajon.

What Do You Need to Know Before Choosing CalHome or SDHC?

Start by clarifying what each program actually covers and where it applies. CalHome is designed for unincorporated areas and targets closing costs directly, while SDHC operates primarily within city limits with larger deferred loan amounts.

- County CalHome

– Use: Closing cost support, generally up to $15,000.

– Structure: Grant with 0 percent interest, deferred for 30 years, typically used to cover appraisal, escrow, and title.

– Best for: Reducing out-of-pocket closing costs in unincorporated areas where you may not qualify for city-only programs.

- SDHC City Programs

– Use: Larger deferred down payment assistance that can also cover some closing costs.

– Size: Often up to $100,000 deferred for eligible buyers, with a citywide purchase price cap around $700,000. A separate middle-income option is commonly up to $50,000 forgivable at 0 percent interest.

– Timeline: Application windows run quarterly, with the next opening April 1, 2026, and funds awarded until exhausted.

– For unincorporated areas: SDHC Home Funds are available in some cases but often capped at $50,000, so confirm property location rules before you apply.

With the inland submarket around $620,000, many first-time buyers target $400,000 to $650,000 condos or townhomes. That matters since some SDHC options cap the purchase at $700,000, while CalHome only targets closing costs, not the full down payment. Your best move in unincorporated areas is often to pair SDHC funds for down payment and supplement with CalHome for any remaining closing costs.

What Do “Grant” and “Deferred” Really Mean?

- Grant: You receive funds for eligible costs and typically do not make monthly payments. CalHome’s closing cost assistance functions as a grant with 0 percent interest and long-term deferment.

- Deferred loan: You receive funds now, make no monthly payments, and repay at sale, transfer, or at term. SDHC programs often use deferred loans, which are larger than CalHome and can cover the down payment plus some closing fees.

- Shared appreciation: Some state programs take a percentage of your future appreciation instead of interest. If you are comparing SDHC and CalHome only, your focus is grant plus deferred, not shared appreciation.

How Do You Compare Your CalHome and SDHC Options?

Match the program design to your specific goal. If your immediate problem is cash to close, CalHome’s targeted closing cost grant up to $15,000 may cover most third-party fees. If you need a larger boost to qualify, SDHC’s deferred loans of $50,000 to $100,000 can bridge the down payment gap and reduce mortgage insurance costs.

Pros of County CalHome

- Dedicated closing cost coverage up to $15,000, which is where many first-time buyers come up short.

- 0 percent interest, long deferment, and no monthly payment, which helps your debt-to-income ratio.

Cons of County CalHome

- Limited to closing costs, so it will not replace your down payment.

- Funding is limited and can be competitive.

Pros of SDHC City Programs

- Larger deferred assistance, often up to $100,000, with some options at $50,000 forgivable.

- Can cover both down payment and a portion of closing costs, which may push you into a better loan tier.

Cons of SDHC City Programs

- Purchase price cap around $700,000 for some programs, which is below the county median.

- Application windows and documentation are more intensive, and property location rules vary for unincorporated areas, where assistance is often capped at $50,000.

Key factors to evaluate:

- Coverage: Do you need pure closing cost coverage, or do you need a larger deferred loan for down payment plus fees?

- Eligibility and location: Does your property sit in an unincorporated area, and does the SDHC option you want allow that address?

- Timing: Can you align your purchase with SDHC’s next application window on April 1, 2026, or do you need a rolling solution?

What Is the Step-by-Step Process for Applying to CalHome and SDHC?

Following a clear sequence prevents missed windows, documentation gaps, and funding conflicts. Here are the ten steps most San Diego first-time buyers should follow when layering these two programs.

1) Confirm your property location. Verify whether the home is in unincorporated San Diego. This determines which SDHC options apply and whether CalHome can be layered.

2) Set your purchase target. Compare a $600,000 to $700,000 price point scenario since many SDHC options cap at about $700,000, while inland median pricing is near $620,000.

3) Get pre-approved with a lender experienced in local assistance. Ask about FHA with 3.5 percent down, conventional with PMI, VA at 0 down, and how assistance affects underwriting.

4) Map your funds. Budget closing costs at roughly 2.5 to 3.0 percent of purchase. At $600,000, that is about $15,000 to $18,000, which aligns with CalHome’s typical cap. Use SDHC deferred funds to augment your down payment and reduce PMI, then stack CalHome to close the remaining fees.

5) Prepare documentation early. Compile W-2s, pay stubs, two months of bank statements, tax returns, and gift letters if any. Assistance programs are document heavy.

6) Calendar the application window. Be ready for SDHC’s April 1, 2026 opening. Some programs award funds first come first served, so timing affects your approval.

7) Run dual approvals. Apply for SDHC and CalHome in parallel if allowed, since layering is often what gets you to the finish line in unincorporated communities.

8) Align your offer with program timelines. Negotiate a 45 to 60 day escrow if possible, which mirrors common processing times seen in local programs.

9) Keep reserves. Maintain a small cushion for prepaid taxes and insurance. Even with assistance, you will want funds for inspection, appraisal re-inspection if needed, and immediate home needs.

10) Lock and re-verify. Lock your rate when advised, and re-verify final numbers with your lender and program administrator before releasing contingencies.

What Does This Look Like for Real Buyers in San Diego?

See the math clearly before you write an offer. Take a $600,000 home in Spring Valley, a common unincorporated target for first-time buyers. Your closing costs at roughly 2.5 to 3.0 percent are about $15,000 to $18,000. County CalHome typically covers up to $15,000 of those fees, which can zero out most third-party costs. If you also secure $50,000 in SDHC assistance in an unincorporated area where capped funds are available, you can apply that to your down payment and reduce mortgage insurance, which helps your monthly DTI in a 6.75 to 7.0 percent rate environment.

If you look at Lakeside or Ramona, you may find similar pricing to the inland median near $620,000. At that level, CalHome still covers the bulk of closing costs, and SDHC can help you bring cash to close down to a more manageable level. If you target a property near the $700,000 cap that applies to some SDHC options, confirm the current cap before submitting your application, since pricing has trended up about 5.6 percent year over year.

This approach also applies if you prefer urban-adjacent areas like Normal Heights or North Park for transit and walkability. Still verify whether the specific address is inside city limits or in an unincorporated pocket. Working with a real estate agent in San Diego who understands program boundaries makes your offer more competitive and helps you navigate neighborhoods that fit first-time budgets, HOA rules, and lifestyle needs.

Neighborhoods to consider in San Diego:

- Spring Valley: Unincorporated, relatively attainable pricing for single-family and townhomes, good access to SR 94 and SR 125.

- Lakeside: Larger lots, suburban feel, similar price points to inland median, attractive for buyers seeking space.

- Normal Heights: Urban amenities and transit, often condo friendly, consider HOA dues and city limit boundaries for program eligibility.

Nearby Areas Worth Exploring

- La Mesa: A small-town main street vibe with Trolley access and stable schools. Pricing often runs a bit higher than Spring Valley but still below many coastal neighborhoods. Preferred if you want walkable dining and quicker commutes to Mission Valley.

- El Cajon: Broad housing stock and its own city down payment assistance program that can reach up to 30 percent of the purchase price, capped around $80,000 as a deferred 0 percent loan, which can outperform SDHC in certain cases.

- Santee: Newer tract homes, parks, and strong freeway access. Pricing can be competitive with Lakeside, with newer townhome communities that fit the first-time buyer budget.

What Mistakes Do Most First-Time Buyers Make With CalHome and SDHC?

The most common mistake is assuming SDHC automatically covers any home in the county, but some programs are city-only or restrict addresses, while unincorporated coverage is often limited or capped near $50,000. Many buyers also believe CalHome replaces their down payment — it does not. CalHome is best viewed as a closing cost grant that complements, not substitutes, your primary loan and any SDHC deferred funds.

Underestimating purchase price caps is another critical error. If you shop well above $700,000, you can price yourself out of some SDHC options and leave assistance on the table. Overlooking timing is equally costly — SDHC opens in cycles, next on April 1, 2026, and funds are competitive. If you wait to assemble documents until you are in escrow, you risk missing your window. Finally, do not rely on one program to do it all. In unincorporated areas, the strongest path is often a layered plan: SDHC for down payment plus CalHome for closing costs, paired with a lender who routinely closes these files and a real estate broker San Diego team that understands location rules.

Frequently Asked Questions

Which program covers more closing costs in unincorporated San Diego?

CalHome generally covers more pure closing costs because it is designed for that purpose, up to about $15,000. SDHC funds can also be used toward closing in some cases, but they are primarily structured as larger deferred down payment loans.

Can you stack County CalHome with SDHC programs?

Yes, you often can, as long as eligibility, property location, and lender guidelines align. A common strategy is to use SDHC for down payment, then layer CalHome to finish closing costs. Confirm stacking rules before submitting your applications.

Does this advice apply to La Mesa or El Cajon too?

Yes, the decision process applies, but programs differ by city. El Cajon offers its own assistance up to 30 percent of the price, capped near $80,000 as a deferred 0 percent loan. In La Mesa, verify whether SDHC or city programs apply, then layer CalHome if available.

How do purchase price caps affect your plan for CalHome or SDHC?

They shape your target list. Some SDHC options cap purchases around $700,000, which is below the county median of $850,000. If you aim near $600,000 to $650,000 in inland areas, you keep more options open and make stacking assistance easier.

When should you apply to SDHC and CalHome in San Diego?

You should prepare now. SDHC windows open quarterly, with the next on April 1, 2026. CalHome funds are limited and can be competitive. You will want your documents ready, lender pre-approval in hand, and property location verified before the window opens.

The Bottom Line

Use County CalHome for what it does best — covering closing costs up to about $15,000 in unincorporated San Diego — while relying on SDHC for larger deferred loans that bridge your down payment and reduce monthly costs. In most unincorporated scenarios, your strongest plan is to stack SDHC assistance, when eligible and capped appropriately, with CalHome to zero out fees, then lock the right first mortgage in today’s 6.75 to 7.0 percent rate environment. Whether you buy in Spring Valley or explore nearby La Mesa and El Cajon, the same principles apply: verify location, confirm caps, time your application, and layer funding to maximize affordability.

If you’re ready to explore your options for CalHome and SDHC in San Diego or nearby communities, reach Scott Cheng at Scott Cheng San Diego Realtor to walk through the specifics for your situation.

📞 858-405-0002

DRE# 01509668

Have Questions About San Diego Real Estate?

Scott Cheng provides free, no-obligation consultations for buyers, sellers, and investors.

Schedule a Consultation